You need to be informed about the cost of your Social Security benefits if you are still working in your twenties or thirties. Your benefits will be lower if you are older. The first year of retirement, your social security benefits will be lower than the ones for the rest of your life.

Benefits of early Retirement

There are several ways to calculate the amount of Social Security benefits you will receive once you retire, including visiting your local Social Security office or creating an account on the official Social Security website. You should know the basics of how benefits are calculated, including AIME/Bend points and PIA. For help with math and determining the best time to retire you can hire a financial adviser.

As an example, let's suppose you were born 1960 and want to retire when you reach 62. Social Security estimates that you'll receive $866 per month once you start claiming benefits at a lower rate. This is about 15 percent less than the benefit you would receive if you retired at full retirement age, which is currently 67. However, you intend to continue working part time to maintain your current standard. This will result a part-time income that is $5,000 higher than your annual earned income limit. If you retire before the age of 65, you'll lose one dollar for each two earnings above the limit. That is roughly $2,500 per year.

Benefits of delaying Social Security

If you're approaching the age of retirement, you may be wondering about the benefits of delaying your Social Security benefits. Although most people believe that delayed benefits mean higher benefits every year, it is often not true. You may see a decrease in your monthly benefits depending on your health and your age.

If you are a woman, it may be worth waiting until you turn 70 to apply for benefits. Reducing your Social Security benefits from 67 to 67 will give you an additional $2,000 per month. But, you'll be penalized by retiring too early. The penalty for early retirement will apply to your entire life. This means that your benefits will be lower in the future than if your benefits were started at 60.

Delaying your decision can increase your benefit

For those who are unable to claim their benefits immediately, Social Security offers several options. You can use a restricted application strategy. If you were born in 1952 or earlier, you can apply to receive your benefits at a later date. This will provide you with more benefits than if you apply early.

Delaying your application can give you an additional 7% to 8.8% increase in benefits every year. Your benefit will be decreased for each $2 you earn. Once you retire at full retirement age, this earnings test will cease to exist.

You get more benefit if you wait to collect

If you are a recent retired person, it could mean that your lifetime Social Security benefits will be more expensive if they are not collected. This can depend on many factors like your health, life expectancy and other sources of income during retirement. It's worth looking into whether it is worth waiting.

Inflation has a definite effect on how much you'll receive each month. Inflation can be particularly detrimental to those with lower incomes. If you're a retiree, it's crucial to protect your savings from rising expenses. You can expect your benefit to increase by approximately 8% if you wait to receive your benefits until 2023.

Tax implications of delaying Social Security

It is important to understand the tax implications of delaying your Social Security payment. Your age and your Social Security rate will determine the amount of tax that you will have to pay. There are ways to reduce the amount of tax you owe. To avoid paying a large tax bill in one lump sum, you could have taxes taken from other income. Another option is to make quarterly payments to the IRS. This decision should be made with the guidance of a tax advisor.

Delaying benefits can lead to a lower monthly check for singles. Benefits can be increased by 8% for those who wait until they reach 66. If you live longer than expected, delay your benefits.

FAQ

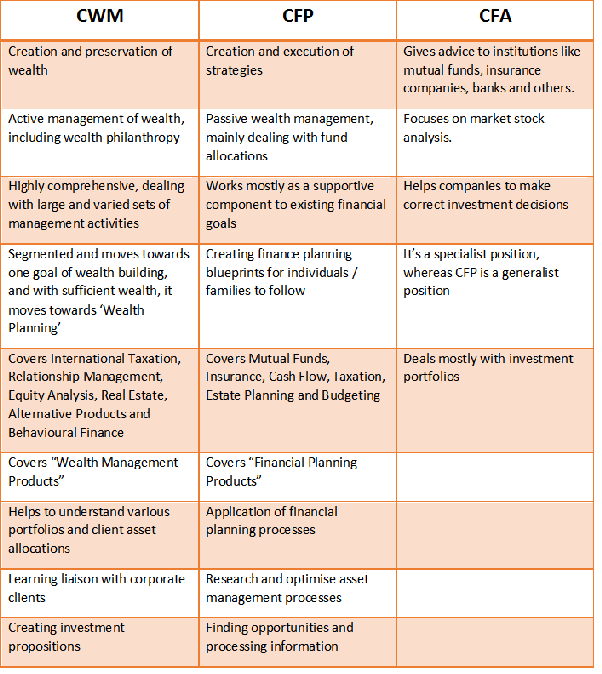

Who should use a wealth manager?

Everybody who desires to build wealth must be aware of the risks.

Investors who are not familiar with risk may not be able to understand it. Poor investment decisions could result in them losing their money.

Even those who have already been wealthy, the same applies. They may think they have enough money in their pockets to last them a lifetime. But they might not realize that this isn’t always true. They could lose everything if their actions aren’t taken seriously.

Everyone must take into account their individual circumstances before making a decision about whether to hire a wealth manager.

What is a Financial Planner? How can they help with wealth management?

A financial advisor can help you to create a financial strategy. A financial planner can assess your financial situation and recommend ways to improve it.

Financial planners, who are qualified professionals, can help you to create a sound financial strategy. They can advise you on how much you need to save each month, which investments will give you the highest returns, and whether it makes sense to borrow against your home equity.

Financial planners typically get paid based the amount of advice that they provide. However, there are some planners who offer free services to clients who meet specific criteria.

How to manage your wealth.

First, you must take control over your money. Understanding your money's worth, its cost, and where it goes is the first step to financial freedom.

It is also important to determine if you are adequately saving for retirement, paying off your debts, or building an emergency fund.

If you don't do this, then you may end up spending all your savings on unplanned expenses such as unexpected medical bills and car repairs.

How to choose an investment advisor

The process of choosing an investment advisor is similar that selecting a financial planer. Experience and fees are the two most important factors to consider.

This refers to the experience of the advisor over the years.

Fees refer to the cost of the service. It is important to compare the costs with the potential return.

It's crucial to find a qualified advisor who is able to understand your situation and recommend a package that will work for you.

Where to start your search for a wealth management service

You should look for a service that can manage wealth.

-

Proven track record

-

Locally based

-

Offers complimentary consultations

-

Continued support

-

There is a clear pricing structure

-

A good reputation

-

It is easy to contact

-

You can contact us 24/7

-

A variety of products are available

-

Low charges

-

Hidden fees not charged

-

Doesn't require large upfront deposits

-

Have a plan for your finances

-

Has a transparent approach to managing your money

-

Allows you to easily ask questions

-

Has a strong understanding of your current situation

-

Understands your goals and objectives

-

Is available to work with your regularly

-

Works within your budget

-

Good knowledge of the local markets

-

Is willing to provide advice on how to make changes to your portfolio

-

Is willing to help you set realistic expectations

Statistics

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

External Links

How To

How to save on your salary

Working hard to save your salary is one way to save. These are the steps you should follow if you want to reduce your salary.

-

You should get started earlier.

-

It is important to cut down on unnecessary expenditures.

-

Online shopping sites like Flipkart, Amazon, and Flipkart should be used.

-

Do not do homework at night.

-

Take care of yourself.

-

Try to increase your income.

-

A frugal lifestyle is best.

-

It is important to learn new things.

-

You should share your knowledge.

-

You should read books regularly.

-

You should make friends with rich people.

-

It's important to save money every month.

-

It is important to save money for rainy-days.

-

Plan your future.

-

Time is not something to be wasted.

-

You must think positively.

-

Negative thoughts should be avoided.

-

God and religion should be given priority

-

Good relationships are essential for maintaining good relations with people.

-

Your hobbies should be enjoyed.

-

Self-reliance is something you should strive for.

-

Spend less than you make.

-

It is important to keep busy.

-

Patient is the best thing.

-

It is important to remember that one day everything will end. It's better if you are prepared.

-

Banks should not be used to lend money.

-

Always try to solve problems before they happen.

-

You should strive to learn more.

-

Financial management is essential.

-

It is important to be open with others.