It can be hard to budget young adults. They need to assess their spending habits and figure out if they're on the right path. If they're on track, they should stick with it. They should establish spending goals and show more discipline with their finances. Here are some tips that will help them get started.

50-30-20 method for budgeting young adults

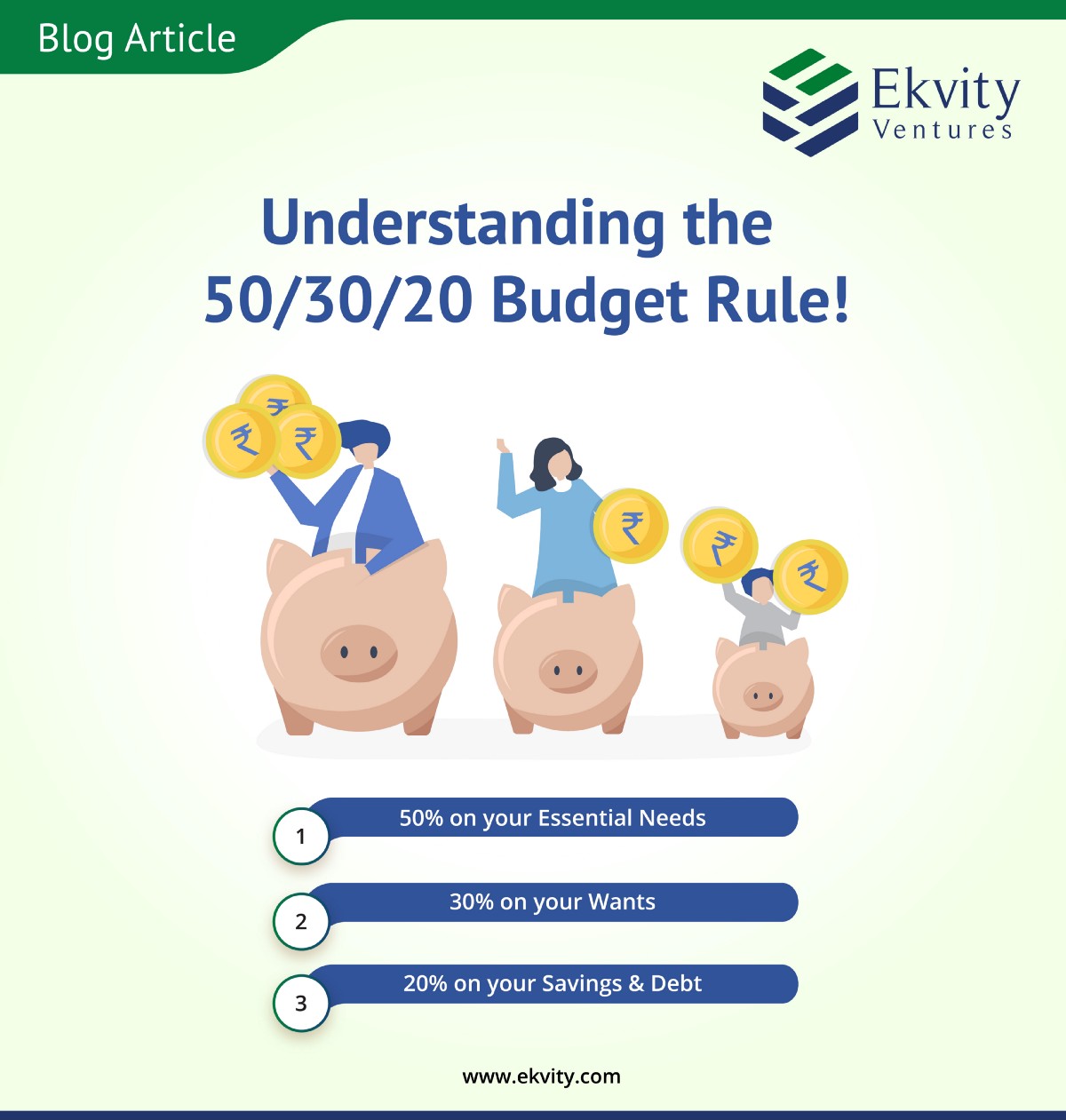

For young adults, the 50/30/20 system for budgeting can be useful in many ways. It will help you determine your needs and preferences and allow you to adjust accordingly. You should set aside 50% for expenses, and 20% for savings or debt payments. This percentage can be adjusted as income fluctuates.

While this method can work well for many people, it is not for everyone. The average American household spends half of its income on essential expenses. A 50/20/30 budget is not practical for many. Still, the method is still useful for people with lower incomes, because it allows you to set aside twenty percent of your monthly budget for goals and investments.

Organize your expenses and prioritize them

Budgeting effectively requires you to organize and prioritize your expenses. Decide what is the most important and what can you cut out from your monthly spending. Begin by organizing all your receipts and keeping track of them. It might take some time, but it will eventually add-up.

After you have organized all of your expenses, you can subtract them from your income to determine what you actually spend each month. If your monthly expenses are less than your income you will have extra money to save, spend or put towards an emergency reserve.

For emergencies, save

You must have emergency funds in case of an unexpected event. This will help you to be able to pay your bills and not lose your job. This money should cover at most three to six months of your daily living expenses. You can increase your emergency fund by cutting back other expenses. Once you have established a goal you can start saving.

An emergency fund should always be separate from your daily expenses. You should have easy access to it without paying any fees. It should have sufficient money to cover the essential living expenses of three to six monthly. It can also be used as a savings account while you search for a new job. The key is to practice discipline. You shouldn't justify buying an expensive gift for an emergency. Also, don't use the fund to purchase flash sales.

FAQ

What Are Some Benefits to Having a Financial Planner?

A financial strategy will help you plan your future. You won't have to guess what's coming next.

It gives you peace of mind knowing that you have a plan in place to deal with unforeseen circumstances.

A financial plan will help you better manage your credit cards. A good understanding of your debts will help you know how much you owe, and what you can afford.

A financial plan can also protect your assets against being taken.

How to Beat Inflation With Savings

Inflation is the rising prices of goods or services as a result of increased demand and decreased supply. Since the Industrial Revolution, people have been experiencing inflation. The government manages inflation by increasing interest rates and printing more currency (inflation). However, there are ways to beat inflation without having to save your money.

For instance, foreign markets are a good option as they don't suffer from inflation. Another option is to invest in precious metals. Since their prices rise even when the dollar falls, silver and gold are "real" investments. Precious metals are also good for investors who are concerned about inflation.

What are the best strategies to build wealth?

It is essential to create an environment that allows you to succeed. It's not a good idea to be forced to find the money. If you're not careful you'll end up spending all your time looking for money, instead of building wealth.

Avoiding debt is another important goal. Although it is tempting to borrow money you should repay what you owe as soon possible.

If you don't have enough money to cover your living expenses, you're setting yourself up for failure. And when you fail, there won't be anything left over to save for retirement.

Before you begin saving money, ensure that you have enough money to support your family.

What is retirement planning?

Financial planning includes retirement planning. It allows you to plan for your future and ensures that you can live comfortably in retirement.

Retirement planning includes looking at various options such as saving money for retirement and investing in stocks or bonds. You can also use life insurance to help you plan and take advantage of tax-advantaged account.

Who can help with my retirement planning

Retirement planning can prove to be an overwhelming financial challenge for many. It's not just about saving for yourself but also ensuring you have enough money to support yourself and your family throughout your life.

The key thing to remember when deciding how much to save is that there are different ways of calculating this amount depending on what stage of your life you're at.

For example, if you're married, then you'll need to take into account any joint savings as well as provide for your own personal spending requirements. Singles may find it helpful to consider how much money you would like to spend each month on yourself and then use that figure to determine how much to save.

You could set up a regular, monthly contribution to your pension plan if you're currently employed. It might be worth considering investing in shares, or other investments that provide long-term growth.

Talk to a financial advisor, wealth manager or wealth manager to learn more about these options.

What is wealth Management?

Wealth Management refers to the management of money for individuals, families and businesses. It encompasses all aspects financial planning such as investing, insurance and tax.

How important is it to manage your wealth?

You must first take control of your financial affairs. You need to understand how much you have, what it costs, and where it goes.

Also, you need to assess how much money you have saved for retirement, paid off debts and built an emergency fund.

This is a must if you want to avoid spending your savings on unplanned costs such as car repairs or unexpected medical bills.

Statistics

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

External Links

How To

How do you become a Wealth Advisor

A wealth advisor is a great way to start your own business in the area of financial services and investing. This profession has many opportunities today and requires many skills and knowledge. These qualities are necessary to get a job. Wealth advisors have the main responsibility of providing advice to individuals who invest money and make financial decisions based on that advice.

First, choose the right training program to begin your journey as a wealth adviser. It should cover subjects such as personal finances, tax law, investments and legal aspects of investment management. And after completing the course successfully, you can apply for a license to work as a wealth adviser.

Here are some tips on how to become a wealth advisor:

-

First, you must understand what a wealth adviser does.

-

You need to know all the laws regarding the securities markets.

-

The basics of accounting and taxes should be studied.

-

After completing your education you must pass exams and practice tests.

-

Finally, you will need to register on the official site of the state where your residence is located.

-

Apply for a license for work.

-

Show your business card to clients.

-

Start working!

Wealth advisors can expect to earn between $40k-60k a year.

The size and geographic location of the firm affects the salary. Therefore, you need to choose the best firm based upon your experience and qualifications to increase your earning potential.

We can conclude that wealth advisors play a significant role in the economy. Everyone should be aware of their rights. They should also know how to protect themselves against fraud and other illegal activities.