You may have heard of the "4% rule", but how do it work? This article will discuss the 4% Rule, how to invest and how you can create a simple budget to fund your retirement. We'll then look at other options for retirement savings such as investing in a brokerage. We'll also discuss Social Security income replacement rates as well as a hypothetical retirement scenario. Once you've identified your retirement deficit you can determine how much you should save to reach it.

4% rule

The 4% retirement savings strategy was developed using historical data spanning 1926 to 1976. Special attention was given to the severe market declines of the 1930s. This approach was meant to allow for inflation, despite the fact that the target inflation rate is only two percent per year. But the current low rate of inflation is making this approach outdated and unsuitable for most investors. Investors should now consider all options, including investments that are both fixed-income and non-fixed-income securities.

Social security income replacement rate

To calculate how much to save for retirement based on your Social Security income replacement rate, you need to know your income before retirement and your current spending levels. Your income replacement rate will decrease the higher your preretirement income. To be on the safe side, you should aim to replace 75% of your income after retirement. Save up to $106,000 if your annual income is $70,000. If you earn less than $70,000, your goal is to replace at least 90%.

Investing in brokerage accounts

Many investors hesitate to put money in a brokerage account as a retirement investment. Unlike an IRA or 401(k), brokerage accounts offer no income or contribution limits. A brokerage account can provide a range of investment opportunities including stocks, bonds, and companies publicly traded that are tied to commodities. Investors should be aware of their risk tolerance and time horizon before they invest.

Creating a simple budget to save for retirement

Before you start retirement savings, create a budget. Compare your monthly income and expenses to determine your budget. Add fun expenses to your budget and save the rest. It will make the transition to retirement much simpler if you have a budget. If you are still working, be sure to refer back to your previous job. Your old job isn't the same without you!

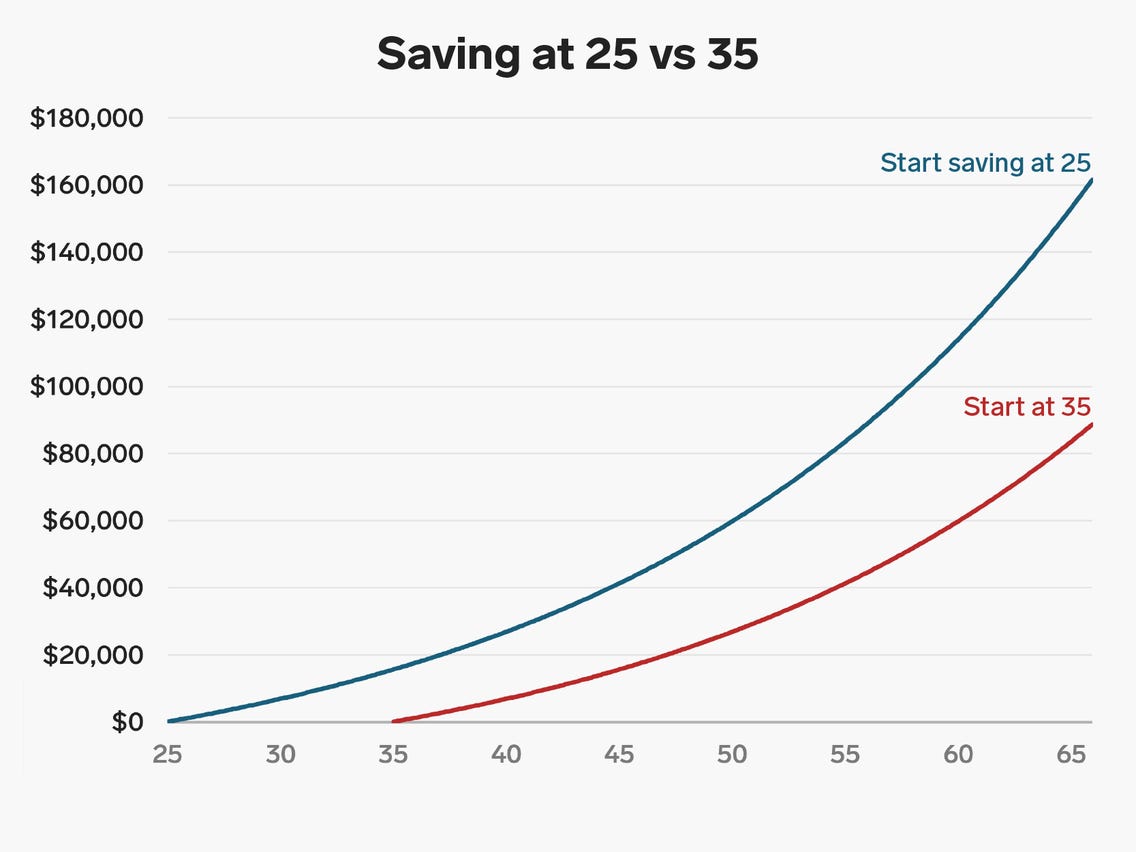

It's time to get serious about retirement savings

It's a great time now to start saving for retirement, even though you may have not thought about it in your early 20s. You might be able to save a little more each month with less to worry about. You might be able save more. So a modest goal of $25 per calendar month in your 20s could make a significant difference for the future. And if you start early enough, you can expect to have enough money by the time you're sixty.

FAQ

What does a financial planner do?

A financial advisor can help you to create a financial strategy. They can help you assess your financial situation, identify your weaknesses, and suggest ways that you can improve it.

Financial planners are professionals who can help you create a solid financial plan. They can tell you how much money you should save each month, what investments are best for you, and whether borrowing against your home equity is a good idea.

Financial planners are usually paid a fee based on the amount of advice they provide. However, there are some planners who offer free services to clients who meet specific criteria.

What are the best ways to build wealth?

You must create an environment where success is possible. You don't want to have to go out and find the money for yourself. If you aren't careful, you will spend your time searching for ways to make more money than creating wealth.

Additionally, it is important not to get into debt. It's very tempting to borrow money, but if you're going to borrow money, you should pay back what you owe as soon as possible.

You are setting yourself up for failure if your income isn't enough to pay for your living expenses. And when you fail, there won't be anything left over to save for retirement.

So, before you start saving money, you must ensure you have enough money to live off of.

How to Choose An Investment Advisor

The process of choosing an investment advisor is similar that selecting a financial planer. There are two main factors you need to think about: experience and fees.

This refers to the experience of the advisor over the years.

Fees are the cost of providing the service. These fees should be compared with the potential returns.

It is essential to find an advisor who will listen and tailor a package for your unique situation.

Statistics

- As of 2020, it is estimated that the wealth management industry had an AUM of upwards of $112 trillion globally. (investopedia.com)

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- According to Indeed, the average salary for a wealth manager in the United States in 2022 was $79,395.6 (investopedia.com)

External Links

How To

How to save money when you are getting a salary

Saving money from your salary means working hard to save money. These are the steps you should follow if you want to reduce your salary.

-

It's better to get started sooner than later.

-

You should reduce unnecessary expenses.

-

Online shopping sites like Flipkart, Amazon, and Flipkart should be used.

-

Do your homework in the evening.

-

It is important to take care of your body.

-

It is important to try to increase your income.

-

It is important to live a simple lifestyle.

-

You should be learning new things.

-

You should share your knowledge.

-

Regular reading of books is important.

-

Rich people should be your friends.

-

You should save money every month.

-

You should save money for rainy days.

-

Plan your future.

-

Do not waste your time.

-

Positive thoughts are best.

-

Negative thoughts should be avoided.

-

God and religion should always be your first priority

-

It is important to have good relationships with your fellow humans.

-

Enjoy your hobbies.

-

Be self-reliant.

-

Spend less than you make.

-

Keep busy.

-

It is important to be patient.

-

Remember that everything will eventually stop. It's better if you are prepared.

-

You should never borrow money from banks.

-

Always try to solve problems before they happen.

-

It is a good idea to pursue more education.

-

You should manage your finances wisely.

-

Be honest with all people